Retention has become one of the biggest challenges for insurance providers today. Whether it is pet insurance, renters insurance, or warranty providers, customers are switching faster than ever.

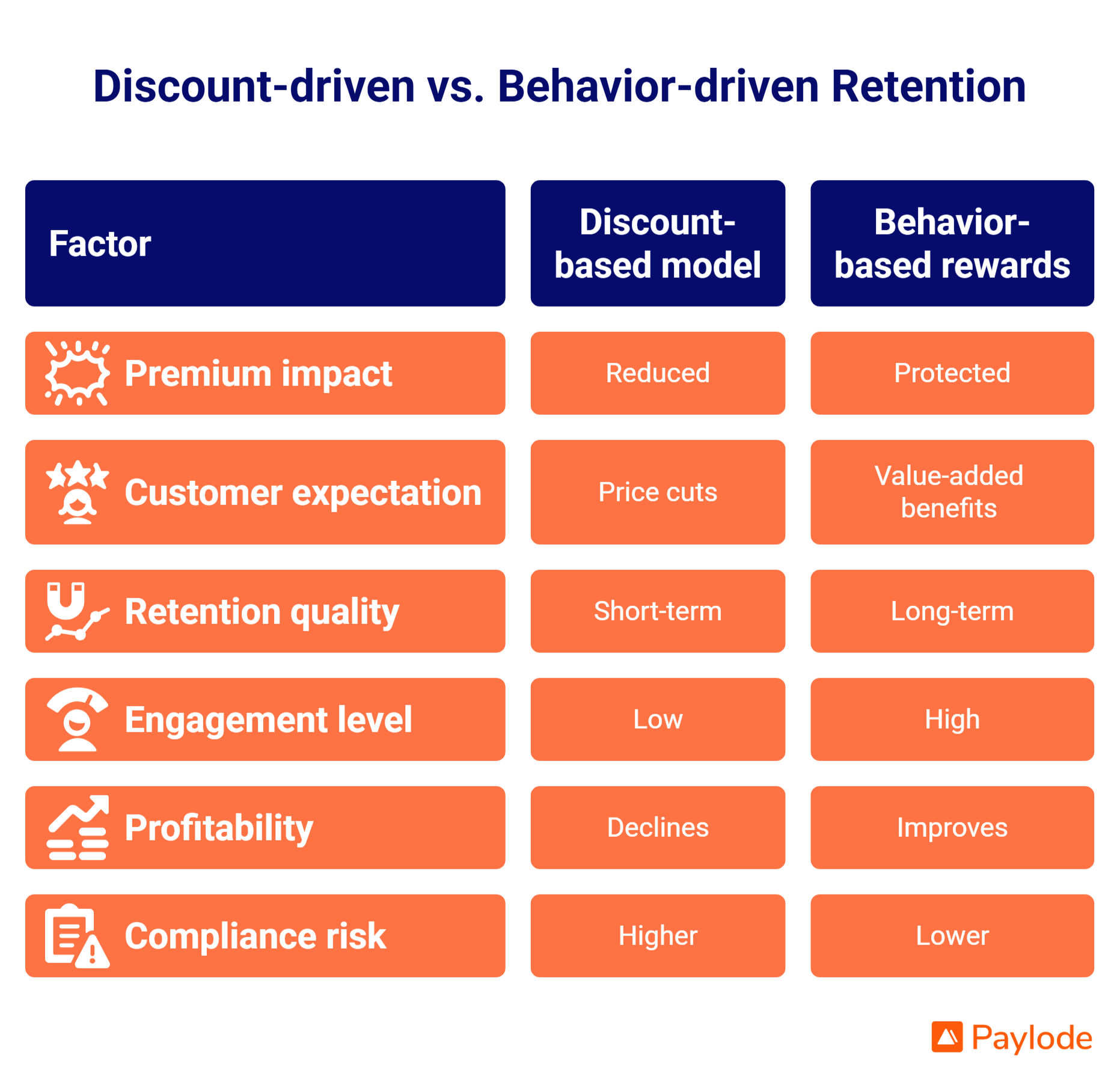

Most companies try to solve this by lowering premiums or offering renewal discounts. But this approach creates a deeper problem. It reduces revenue, weakens brand value, and trains customers to wait for the next offer.

Insurance leaders are now looking for smarter ways to increase insurance retention without touching pricing. The focus is shifting from price reduction to value creation.

Customers no longer stay just because a policy is cheaper. They stay because they feel they are getting consistent value throughout their journey.

This is where behavior-based engagement comes in. Instead of offering discounts, insurers reward actions like:

- Paying on time

- Renewing early

- Staying engaged with the platform

- Choosing digital interactions

This approach helps insurance companies build stronger relationships while protecting premium integrity.

For example, many providers are now encouraging digital behavior such as paperless billing and automated engagement journeys, similar to how insurers can drive adoption through switch to paperless experiences.

The result is simple but powerful:

- Customers feel rewarded, not discounted

- Engagement increases across the lifecycle

- Retention improves without reducing price

In today’s market, the goal is not just to retain customers—it is to retain them profitably and consistently.

And the companies that succeed will be the ones that shift from discounting to delivering everyday value.

1. Why rebates and discounts are not sustainable

At first glance, discounts seem like an easy way to retain customers. Lower the price, and customers stay.

But in reality, this approach creates long-term challenges that make it harder to increase insurance retention in a healthy and scalable way.

Instead of building loyalty, discounts often weaken both profitability and customer behavior over time.

1.1 Margin pressure and profitability risk

Discounts directly reduce the value of each policy. While this may improve short-term retention, it comes at the cost of long-term revenue.

Over time, this creates a compounding impact:

- Lower customer lifetime value

- Reduced ability to invest in a better customer experience

- Increased dependency on ongoing incentives

More importantly, discounts are hard to reverse.

Once customers get used to lower premiums, removing those discounts can lead to dissatisfaction and churn. What starts as a temporary tactic quickly becomes a permanent expectation.

1.2 Regulatory and compliance limitations

Insurance is a regulated industry, and pricing changes cannot be made freely.

Discount strategies often face limitations such as:

- Strict approval processes for pricing adjustments

- Rules around fair and consistent pricing

- Risk of non-compliance with uneven discounting

This makes it difficult to scale discount-based retention strategies across different customer segments.

Instead of flexibility, insurers face restrictions that slow down growth and innovation.

1.3 Customer conditioning problem

One of the biggest hidden risks of discounts is how they shape customer behavior.

When customers expect discounts, their mindset changes:

- They delay renewals, waiting for better offers

- They compare prices more frequently

- They become less loyal and more price-sensitive

This creates a cycle where insurers must continue offering discounts just to maintain retention levels.

In the long run, this does not build loyalty—it builds dependency.

Discounts may provide short-term relief, but they do not create lasting customer relationships.

To truly increase insurance retention, insurers need to move beyond pricing tactics and focus on delivering consistent, everyday value that keeps customers engaged throughout their journey.

2. What customers actually want from insurance providers

To truly increase insurance retention, insurance companies need to rethink what customers value.

Retention is no longer driven by price alone. Customers expect more than just coverage—they expect ongoing value throughout their relationship with the provider.

2.1 Value beyond claims

Traditionally, insurance has been a low-engagement product. Customers interact only when they file a claim or renew a policy.

But today’s customers expect more frequent value. They want benefits that show up in their daily lives, not just during rare events.

This shift is clear:

- From one-time interaction → to ongoing engagement

- From reactive service → to proactive value

Insurance providers that deliver everyday benefits are more likely to stay top of mind and improve retention.

2.2 Emotional drivers of retention

Retention is not just about logic—it is also about how customers feel.

Three key emotional drivers influence whether a customer stays or switches:

Trust

Customers want to feel confident that their provider is reliable and consistent. Trust builds over time through positive experiences, not just pricing.

Convenience

Simple, frictionless experiences matter. Easy payments, digital access, and quick support all contribute to higher retention.

Ongoing benefits

Customers are more likely to stay when they feel they are getting continuous value—not just paying for a service they rarely use.

These emotional factors play a bigger role in retention than discounts ever can.

2.3 Industry-specific expectations

Different insurance segments have unique customer expectations. Understanding these differences is key to designing effective retention strategies.

Pet insurance

Pet owners look for value that supports their pet’s everyday well-being. This includes:

- Wellness-related perks

- Discounts on pet food, grooming, and care services

These benefits create frequent touchpoints beyond claims.

Renters insurance

Renters expect benefits that align with their lifestyle and mobility.

- Lifestyle perks that enhance daily living

- Moving-related benefits that reduce friction during transitions

These experiences make the insurance provider more relevant in everyday life.

Warranty providers

Warranty customers value convenience and peace of mind.

- Maintenance support to extend product life

- Easy replacement or repair experiences

The easier it is to manage and maintain products, the more likely customers are to renew.

Understanding what customers truly want allows insurance companies to design better engagement strategies.

And when customers experience consistent value across their journey, it becomes much easier to increase insurance retention - without relying on discounts.

3. The shift to behavior-based retention strategies

To truly increase insurance retention, insurance companies are moving away from discounts and toward a more sustainable approach—behavior-based rewards.

This model is simple. Instead of lowering the price, insurers reward customers for specific actions that strengthen their relationship with the brand.

It shifts the focus from cost reduction to value creation.

Customers are not staying because the policy is cheaper. They are staying because they are actively engaged and consistently rewarded.

3.1 Key behaviors to incentivize

The success of this model depends on identifying the right customer actions to reward. These are behaviors that directly impact retention and long-term value.

1. On-time payments

Encouraging timely payments improves consistency and reduces risk, while also reinforcing positive habits.

2. Policy renewals

Rewarding renewals shifts the focus from price comparison to loyalty and continued engagement.

3. Digital engagement

Customers who interact with apps, portals, or communications are more likely to stay connected with the brand.

4. Add-on purchases

Cross-sell and add-ons increase customer value while deepening the relationship.

By aligning rewards with these behaviors, insurers create a system where both the business and the customer benefit.

3.2 Why this model works

Behavior-based rewards are effective because they influence how customers interact with the insurance provider over time.

1. Builds habit loops

When customers are rewarded for actions, those actions become routine. Over time, this creates consistent engagement.

2. Keeps customers engaged throughout the policy lifecycle

Instead of interacting only at renewal, customers stay connected through multiple touchpoints across the year.

3. Protects premium pricing

Unlike discounts, this model does not reduce the base price. It maintains pricing integrity while still delivering value.

This shift is helping insurance providers move from reactive retention strategies to proactive engagement models.

And the result is clear—when customers are consistently engaged and rewarded, it becomes much easier to increase insurance retention without relying on discounts.

4. How behavior-based rewards increase insurance retention

Behavior-based rewards are not just a different strategy—they fundamentally change how customers interact with insurance providers.

Instead of focusing only on renewal moments, this approach builds continuous engagement across the entire customer journey.

This is what makes it highly effective in helping insurers increase insurance retention without relying on discounts.

4.1 Creates continuous engagement

Traditional insurance models are built around a single key moment—renewal.

But behavior-based rewards shift this dynamic. They create multiple touchpoints throughout the year.

- Customers engage beyond policy start and renewal

- Interactions become more frequent and meaningful

- The relationship stays active, not dormant

This moves insurance from a “once-a-year renewal” experience to an ongoing interaction model.

4.2 Strengthens perceived value

One of the biggest drivers of retention is how much value customers feel they are getting.

With behavior-based rewards:

- Customers receive benefits regularly

- The experience feels more rewarding without lowering premiums

- Value becomes visible and consistent

Instead of asking, “Is this policy cheaper elsewhere?”, customers start thinking, “I get more value here.”

4.3 Reduces churn triggers

Discount-driven models often push customers to compare prices.

Behavior-based models reduce this tendency by shifting focus away from cost.

- Less emphasis on price comparison

- More focus on the overall benefits of the ecosystem

- Stronger emotional connection with the provider

When customers see ongoing value, they are less likely to switch—even if a cheaper option exists.

This is why leading insurance providers are adopting behavior-based engagement models.

They do not just retain customers—they build stronger, longer-lasting relationships that make it easier to increase insurance retention in a sustainable way.

5. Use cases across insurance segments

Behavior-based rewards are not one-size-fits-all. To effectively increase insurance retention, insurers need to tailor rewards based on the specific needs of each segment.

Different insurance categories have different customer expectations, and aligning rewards with those expectations drives stronger engagement.

5.1 Pet insurance

Pet owners are highly engaged and emotionally connected to their pets. This creates an opportunity for frequent, value-driven interactions.

Insurance providers can:

- Reward vet visits and wellness checkups

- Offer pet care perks such as grooming, food, and preventive care

These benefits create ongoing touchpoints and make the insurance provider part of the pet’s everyday care journey.

5.2 Renters insurance

Renters value convenience, flexibility, and digital-first experiences.

Insurance providers can improve retention by encouraging behaviors like paperless billing and responsible usage. For example, insurers can drive adoption through switch to paperless programs that reward digital engagement.

Additional strategies include:

- Rewarding safe behavior such as home safety practices

- Incentivizing timely payments and consistent engagement

These actions make the insurance experience more seamless and relevant to everyday life.

5.3 Warranty providers

Warranty customers prioritize ease and reliability.

Behavior-based rewards can support this by encouraging:

- Product registrations for better tracking and service

- Renewals and upgrades through ongoing incentives

This approach reduces friction and ensures customers stay connected to the provider throughout the product lifecycle.

When rewards are aligned with real customer needs, they become more meaningful and effective.

This is how insurance providers can create segment-specific strategies that consistently increase insurance retention while delivering real value to customers.

6. Lifecycle-based engagement model

To effectively increase insurance retention, insurers need to engage customers at every stage of their journey—not just at renewal.

A lifecycle-based approach ensures that customers receive consistent value from the moment they sign up to the moment they renew.

This creates a stronger relationship and reduces the chances of churn.

6.1 Onboarding stage

The first few weeks are critical in shaping customer perception.

This is the best time to introduce value and build early engagement.

Insurance providers can:

- Offer welcome perks to create a strong first impression

- Reward early actions, such as account setup or first interaction

Early engagement sets the tone for the entire customer lifecycle.

6.2 Active policy stage

This is the longest phase of the customer journey, and often the most underutilized.

Instead of staying inactive, insurers can create regular engagement opportunities.

- Provide monthly or quarterly rewards

- Encourage digital interactions such as app usage or communication engagement

Consistent interaction ensures the brand stays relevant throughout the policy period.

6.3 Renewal stage

Traditionally, renewal is where discounts are applied. But this is also where behavior-based strategies create the most impact.

- Reward loyalty instead of lowering premiums

- Reinforce the value already delivered throughout the year

When customers recognize the benefits they have received, they are more likely to renew without needing a discount.

A lifecycle-based engagement model ensures that customers are continuously connected with the insurance provider.

And when value is delivered at every stage, it becomes much easier to increase insurance retention in a sustainable and scalable way.

7. How to implement a rewards-driven retention strategy

Shifting to a rewards-driven model requires a structured approach. Insurance companies that follow a clear framework are better positioned to increase insurance retention while maintaining operational efficiency.

The goal is simple - align customer actions with meaningful rewards and deliver them consistently.

7.1 Step 1: Identify key customer behaviors

Start by identifying the actions that directly impact retention and long-term value.

These typically include:

- Payments (especially on-time payments)

- Policy renewals

- Engagement actions such as app usage or communication interaction

Focusing on the right behaviors ensures that rewards drive measurable outcomes.

7.2 Step 2: Map rewards to behaviors

Once behaviors are defined, the next step is to assign relevant rewards.

The key insight here is that smaller, frequent rewards are more effective than large, one-time discounts.

- They create consistent engagement

- They reinforce positive behavior over time

- They feel more achievable and motivating to customers

This approach builds long-term habits instead of short-term reactions.

7.3 Step 3: Automate delivery

Manual reward systems are difficult to scale and maintain.

To ensure consistency and efficiency, insurers should automate reward delivery through integrated systems.

- Connect rewards with billing platforms

- Integrate with CRM systems for personalized experiences

- Ensure rewards are triggered in real time based on customer actions

Automation makes the entire process seamless for both the business and the customer.

7.4 Step 4: Measure performance

To continuously improve the strategy, insurers must track the right metrics.

Key performance indicators include:

- Retention rate

- Engagement rate

- Customer lifetime value

These metrics help determine what is working and where improvements are needed.

A well-implemented rewards strategy turns everyday customer actions into opportunities for engagement.

And when done right, it becomes a powerful way to increase insurance retention without relying on discounts or pricing changes.

8. Role of platforms in scaling retention

As insurance companies grow, managing rewards and engagement manually becomes difficult.

What works for a small customer base quickly breaks at scale. This is why platforms play a critical role in helping insurers increase insurance retention efficiently.

Manual rewards programs often fail for a few key reasons:

- Inconsistent reward delivery

- Limited personalization

- High operational effort

- Delayed customer engagement

These challenges reduce the effectiveness of even the best retention strategies.

To solve this, insurance providers need systems that can automate and personalize engagement at scale.

Modern platforms enable insurers to:

- Automatically trigger rewards based on customer behavior

- Personalize experiences across different customer segments

- Deliver consistent value throughout the lifecycle

For example, insurers can use the Paylode platform to manage and automate reward-driven engagement across their customer base.

They can also enhance customer experience by offering curated benefits through perks and rewards programs that align with everyday needs.

To further improve engagement, solutions like Boost engagement help drive higher interaction and participation across key touchpoints.

By combining automation with personalization, platforms make it easier to deliver consistent value without increasing operational complexity.

This allows insurance companies to scale their retention strategies while maintaining quality and relevance.

In a competitive market, the ability to deliver the right reward at the right time can make all the difference.

And with the right platform in place, insurers can consistently increase insurance retention while building stronger customer relationships.

9. Measuring success: KPIs that matter

To effectively increase insurance retention, it is important to track the right performance indicators.

A rewards-driven strategy should not just feel effective - it should be measurable and continuously optimized based on real data.

Retention rate improvement

This is the most direct indicator of success.

- Measure how many customers stay over time

- Compare retention before and after implementing rewards

- Track improvements across different customer segments

Even small percentage increases can lead to significant long-term revenue gains.

Renewal conversion rate

Renewal is a critical moment in the customer lifecycle.

- Track how many customers renew without requiring discounts

- Measure the impact of rewards on renewal decisions

- Identify which behaviors lead to higher renewal rates

A higher renewal conversion rate indicates stronger customer loyalty.

Engagement frequency

Engagement is a leading indicator of retention.

- Monitor how often customers interact with your platform

- Track actions like logins, clicks, and reward redemptions

- Identify patterns that correlate with long-term retention

More frequent engagement typically leads to stronger relationships and lower churn.

Cost vs retention ROI

It is important to balance investment with outcomes.

- Compare the cost of rewards programs with retention gains

- Evaluate savings from reduced churn

- Measure overall impact on customer lifetime value

Unlike discounts, which reduce revenue directly, rewards can deliver higher returns without affecting pricing.

By focusing on these key metrics, insurance companies can build a data-driven approach to retention.

This ensures that every effort is aligned with the goal to increase insurance retention in a sustainable and scalable way.

10. Common mistakes to avoid

Common mistakes to avoid

While behavior-based strategies are effective, execution plays a critical role.

Insurance companies that overlook key details may struggle to see results, even with the right approach. Avoiding these common mistakes is essential to successfully increase insurance retention.

Over-rewarding without strategy

Offering too many rewards without a clear plan can reduce their impact.

- Customers may start to expect rewards for every action

- Costs can increase without meaningful improvement in retention

- The program loses focus and effectiveness

Rewards should be tied to specific behaviors that drive long-term value.

One-size-fits-all rewards

Not all customers are the same. Treating them the same reduces engagement.

- Different segments have different needs

- Generic rewards may feel irrelevant

- Personalization is key to making rewards meaningful

Tailored experiences create stronger connections and better outcomes.

Ignoring lifecycle stages

Focusing only on one stage—such as renewal—limits the effectiveness of the strategy.

- Engagement should start from onboarding

- Continue through the active policy period

- Strengthen at renewal

A full lifecycle approach ensures consistent value delivery.

Not communicating benefits clearly

Even the best rewards program will fail if customers do not understand it.

- Customers need to know what they are getting

- Clear communication increases participation

- Visibility drives perceived value

Simple and consistent messaging makes rewards more impactful.

Avoiding these mistakes helps insurance providers build a stronger, more effective retention strategy.

When rewards are thoughtful, personalized, and well-communicated, they become a powerful tool to increase insurance retention without relying on discounts.

11. Future of insurance retention

Future of insurance retention

The future of insurance retention is not built on pricing strategies. It is built on relationships.

As customer expectations continue to evolve, insurance providers must move beyond transactional interactions and focus on creating long-term engagement. This shift is essential to sustainably increase insurance retention.

Shift from transactional to relationship-driven models

Traditional insurance models are transactional. Customers pay premiums and interact only when necessary.

But the future is relationship-driven.

- Continuous engagement replaces one-time interactions

- Value is delivered throughout the customer journey

- Loyalty is built through consistent experiences

This approach strengthens trust and keeps customers connected over time.

Embedded perks ecosystems

Insurance is becoming part of a larger value ecosystem.

Instead of offering standalone policies, providers are integrating perks and benefits into everyday life.

- Lifestyle benefits that customers use regularly

- Partnerships that extend value beyond insurance

- Always-on rewards that keep customers engaged

These ecosystems make insurance more relevant and harder to replace.

Personalization at scale

Customers expect experiences tailored to their needs.

With the right technology, insurers can:

- Deliver personalized rewards based on behavior

- Customize engagement across different segments

- Scale experiences without increasing complexity

Personalization makes every interaction more meaningful and effective.

The future belongs to insurance providers who can combine engagement, personalization, and value into one seamless experience.

And those who adapt to this model will find it much easier to increase insurance retention while building stronger, more loyal customer relationships.

Conclusion: retention without reducing premiums

Insurance companies no longer need to rely on discounts to retain customers.

While rebates may deliver short-term results, they weaken long-term value and create unsustainable expectations. The smarter approach is to focus on consistent, meaningful engagement that keeps customers connected throughout their journey.

To truly increase insurance retention, insurers must shift their strategy:

- From price reduction to value creation

- From one-time interactions to continuous engagement

- From generic offers to personalized experiences

When customers receive ongoing benefits, they feel valued—not incentivized to leave.

FAQs

1. How can insurance companies increase retention without discounts?

Insurance companies can increase retention by using behavior-based rewards that encourage engagement, such as rewarding on-time payments, renewals, and digital interactions.

2. What are behavior-based rewards in insurance?

Behavior-based rewards are incentives given to customers for specific actions, helping build engagement and loyalty without lowering premiums.

3. Why are discounts not effective for long-term retention?

Discounts reduce profitability and train customers to expect lower prices, which weakens long-term loyalty.

4. Do rewards programs really help increase insurance retention?

Yes, rewards programs improve engagement and perceived value, which leads to higher retention rates over time.

5. Which insurance segments benefit most from rewards?

Pet insurance, renters insurance, and warranty providers benefit the most due to their ability to create frequent customer touchpoints.

.jpg)